Table of Contents

Why You Are Probably Leaving Money on the Table

The IRS processed over 162 million individual tax returns in 2024, and the Government Accountability Office estimates that taxpayers overpay by roughly $1 billion annually due to missed deductions and credits. That is not because the tax code is impossible to understand. It is because most people use tax software, answer the basic prompts, and accept whatever number appears at the bottom of the screen. The software only searches for deductions you tell it to search for. If you do not know a deduction exists, the software will not find it for you.

The shift away from itemizing makes this problem worse. After the Tax Cuts and Jobs Act of 2017 roughly doubled the standard deduction, the share of taxpayers who itemize dropped from about 30% to around 10%, according to the Tax Foundation. But millions of taxpayers in that 10% are still leaving itemized deductions unclaimed. And even more taxpayers miss above-the-line deductions, which reduce your adjusted gross income whether you itemize or take the standard deduction. These are the gold mine.

The practical rule: tax deductions come in two flavors. Above-the-line deductions lower your AGI and are available to everyone. Itemized deductions replace the standard deduction but only make sense if their total exceeds the standard deduction amount. Know which bucket each deduction lives in, and do not ignore either one.

Above-the-Line Deductions That Everyone Can Claim

Above-the-line deductions are the most underutilized tax breaks because they do not require you to itemize. The student loan interest deduction lets you deduct up to $2,500 of interest paid on qualified student loans, and it phases out at higher incomes. In 2026, the phase-out begins at $80,000 for single filers and $165,000 for married couples filing jointly. According to the U.S. Department of Education, roughly 40% of eligible borrowers fail to claim this deduction each year. If you paid $1,500 in student loan interest and are in the 22% bracket, that deduction saves you $330. The lender sends Form 1098-E each January. Do not toss it in the junk mail pile.

Financial Fact: The IRS reports that the average tax refund is over $3,000. Adjusting your W-4 to reduce your refund by $250 per month puts that money in your pocket year-round instead of giving the government an interest-free loan.

Health Savings Account contributions are deductible above the line. In 2026, an individual with a high-deductible health plan can deduct up to $4,150 in HSA contributions. A family plan allows up to $8,300. Every dollar you contribute reduces your taxable income, and when you use the money for qualified medical expenses, the withdrawals are tax-free. About 35% of HSA-eligible individuals do not contribute to their HSA at all, according to the Employee Benefit Research Institute. If you have a qualifying health plan, even a $100 monthly contribution is worth making.

Traditional IRA contributions may be fully or partially deductible depending on your income and whether you or your spouse has a workplace retirement plan. A single filer covered by a workplace plan can deduct the full $7,000 contribution if modified AGI is $79,000 or less in 2026. The deduction phases out completely at $89,000. Many people mistakenly believe IRA contributions are not deductible once you have an employer plan. That is only true above certain income thresholds. Check IRS Publication 590-A for your specific numbers. The practical move: log into your HSA right now and increase contributions by even $50 per month. Then check whether your IRA contribution is deductible based on your latest AGI.

Itemized Deductions Hiding in Plain Sight

If your total itemized deductions exceed the standard deduction ($15,000 for single filers and $30,000 for married couples filing jointly in 2026), you should itemize. Medical and dental expenses are deductible to the extent they exceed 7.5% of your AGI. A single filer earning $80,000 with $10,000 in unreimbursed medical expenses can deduct $4,000. Health insurance premiums paid with after-tax dollars, long-term care insurance premiums up to age-based limits, and mileage to and from medical appointments at $0.21 per mile all count. According to a 2023 analysis by the Kaiser Family Foundation, roughly 17% of adults have out-of-pocket medical expenses exceeding $2,000 annually. Many of them do not track or claim these costs.

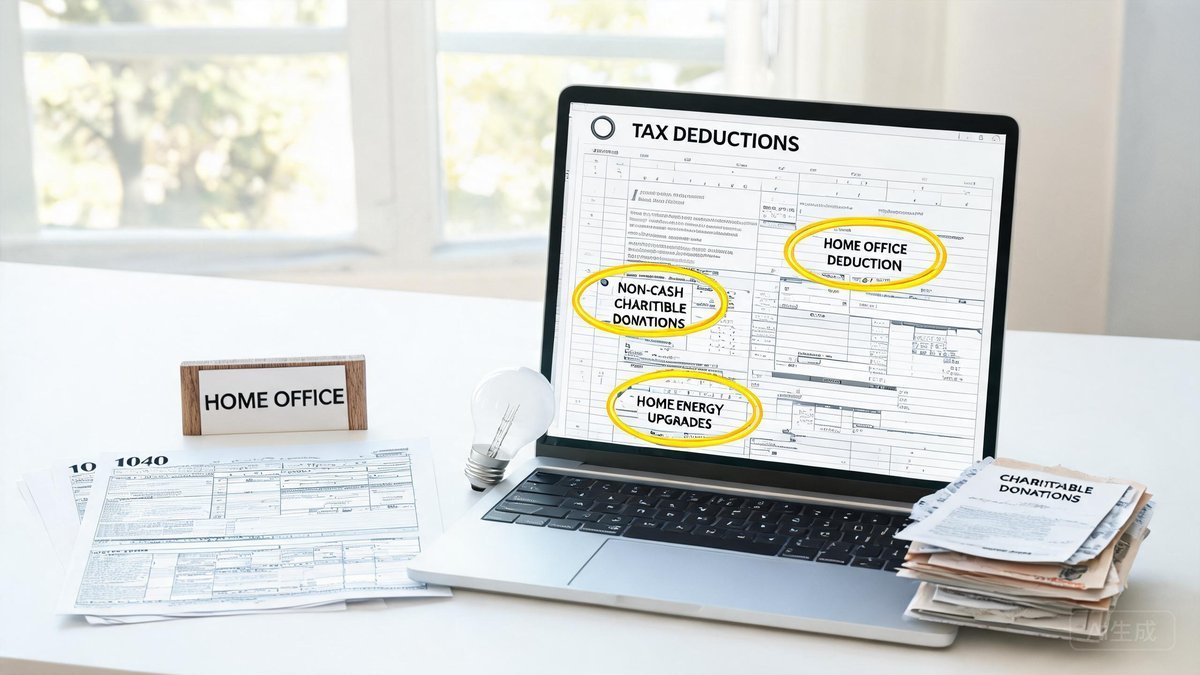

State and local taxes are deductible up to $10,000 combined for property taxes and either state income tax or state sales tax. If you live in a state with no income tax, like Texas or Florida, you can deduct state and local sales tax instead. The IRS provides a calculator and optional tables based on your income and location, or you can save receipts and claim the actual amount paid. If you bought a car or made another large purchase subject to sales tax, the actual method almost always produces a higher deduction than the table.

Charitable contributions count whether you write a check, donate appreciated stock, or drive for a nonprofit. The mileage rate for charitable driving is $0.14 per mile. Small donations add up: $25 monthly to a food bank equals $300 annually, all deductible if you itemize. The practical move: before you file, add up your medical expenses, your state tax payments, your mortgage interest, and your charitable contributions. If the total beats the standard deduction, itemize. If you are close, look for additional qualifying expenses you may have missed.

Credits That Put Cash Directly in Your Pocket

Tax credits are better than deductions. A deduction reduces your taxable income. A credit reduces your tax bill dollar for dollar. A $1,000 credit is worth $1,000. A $1,000 deduction in the 22% bracket is worth $220. The Earned Income Tax Credit is the most powerful credit for low-to-moderate-income workers, worth up to $7,830 in 2026 for a family with three or more qualifying children. Yet the IRS estimates that one in five eligible taxpayers fails to claim it, often because they do not know they qualify or because their income changed and they did not update their filing.

The Child and Dependent Care Credit covers 20% to 35% of up to $3,000 in care expenses for one dependent or $6,000 for two or more. If you work and pay for child care, summer day camp, or after-school programs, those costs count. The Child Tax Credit provides up to $2,000 per qualifying child under 17, with up to $1,700 refundable as the Additional Child Tax Credit. The income phase-out begins at $200,000 for single filers and $400,000 for married couples, so most middle-class families qualify for the full amount.

The Saver's Credit, formally the Retirement Savings Contributions Credit, rewards low-to-moderate-income workers who contribute to an IRA or workplace retirement plan. It is worth up to $1,000 for single filers and $2,000 for married couples, and it is in addition to the deduction or Roth benefit you already get from the contribution itself. In 2026, single filers with AGI up to $23,750 qualify for the maximum 50% credit on contributions up to $2,000. The practical move: check the income limits for the EITC and the Saver's Credit every year, even if you did not qualify previously. Inflation adjustments shift the thresholds upward annually.

Self-Employed and Investment Deductions Worth Knowing

If you are self-employed or run a small side hustle, the home office deduction is legitimate and valuable. To qualify, you must use a portion of your home regularly and exclusively for business. The simplified method gives you $5 per square foot up to 300 square feet, for a maximum deduction of $1,500. The regular method lets you deduct a percentage of actual expenses including mortgage interest, property taxes, utilities, and repairs based on the percentage of your home used for business. If your home office is 10% of your home's square footage, you deduct 10% of those household expenses.

Self-employed health insurance premiums covering yourself, your spouse, and your dependents are deductible above the line, even if you do not itemize. This deduction does not require you to have a formal business entity. Sole proprietors, LLC members, and partners all qualify. And it applies to dental and long-term care insurance premiums as well.

On the investment side, interest paid on margin loans is deductible as investment interest expense up to the amount of your net investment income. If you pay $3,000 in margin interest and earn $3,000 in interest and dividends, the entire margin interest is deductible if you itemize. You can also deduct advisory fees and safe deposit box fees in certain circumstances, though these are more limited after recent tax law changes. The practical rule: if you have self-employment income, track every business-related expense contemporaneously using an app or spreadsheet. If you invest on margin, review your Form 1099 for interest expense that qualifies for the deduction.

Building a robust savings habit is the foundation of financial independence, yet most people never develop a systematic approach to saving. The most effective strategy is to automate your savings so the money moves out of your checking account before you have a chance to spend it. Setting up an automatic transfer on payday to a dedicated savings account removes the willpower element entirely. Financial advisors typically recommend saving at least 15 to 20 percent of your gross income for long-term goals. If that seems impossibly high, start with 5 percent and increase it by one percentage point every three months. The gradual ramp-up is barely noticeable in your daily spending but produces dramatic results over a working career due to the power of compound growth.